02 Feb Money Thoughts – Q1 2026

The DLD Financial Q1 2026 newsletter highlights the upcoming RRSP contribution deadline, offering practical guidance on contribution strategies, tax planning, and key programs like spousal RRSPs and FHSAs. It also shares Fidelity’s 2026 market outlook, covering AI, global diversification, Canada’s improving fundamentals, and alternative investments, alongside insights on the value of an advisor, tax-efficient investing, and DLD’s recent media features.

The DLD Financial Q1 2026 newsletter highlights the upcoming RRSP contribution deadline, offering practical guidance on contribution strategies, tax planning, and key programs like spousal RRSPs and FHSAs. It also shares Fidelity’s 2026 market outlook, covering AI, global diversification, Canada’s improving fundamentals, and alternative investments, alongside insights on the value of an advisor, tax-efficient investing, and DLD’s recent media features.

RRSP Contribution Deadline for 2025 taxes – March 2, 2026

We are now just about 5 weeks away from the RRSP contribution deadline of March 02, 2026 for the 2025 tax year. Below are some quick refreshers on RRSPs:

RRSP contribution eligibility:

– Anyone who has earned income and filed a tax return can contribute until Dec 31 of the year they turn age 71

– Spousal RRSPs can be used until Dec 31 of the year the spouse turns age 71

Should you be using or topping up your RRSPs?

If you’re not sure, please get in touch ASAP to further discuss your specific situation by booking a short, 20-minute virtual meeting in your advisor’s calendar.

Contribution limits and where you find your limit:

The annual RRSP contribution limit is the lower of 18% of your earned income from the previous year or the maximum annual contribution limit coupled with unused contribution room from past years. RRSP contribution room can be carried forward to subsequent years if you don’t maximize your room this year. There is also a one-time $2000 lifetime over-contribution allowance but note that this amount is not tax deductible.

> View chart indicating the maximums on past years

> For your personal contribution limit, please check your most recent Notice of Assessment from CRA

The power of Dollar-cost averaging:

We are huge advocates of automating your long-term savings contributions as it’s one of the best ways for forced savings. Dollar-cost averaging means you buy more units when the prices are low and less units when prices are high.

Spousal RRSP:

This strategy makes sense for spouses where one spouse earns more than the other spouse. This allows for the higher-income spouse to deduct the contribution on their taxes and for the lower-income spouse to own the RRSP. This is a great way to be proactive about future income splitting.

RRSP Contribution Calculator:

A common question we often get is “How much of a ‘refund’ will I receive based on a certain dollar value?” Here is a calculator that will help calculate the approximate tax savings from the RRSP contribution.

First Time Home Buyer’s Plan (FHP) and Lifelong Learning Plan (LLP)

If you have taken advantage of one or both of these programs, please remember to contribute and allocate the specified amount as noted on your notice of assessment when you file your taxes. Otherwise, the repayment amount will be added to your income. For example, if you took out funds in 2019 to purchase your first home, your first repayment is due for the 2021 tax year and you have 15 years to repay what you took out.

**RRSP withdrawals taken from January 01, 2022 to December 31, 2025 will have a 5 year grace period before repayment is required.**

For the lifelong learning plan, you also have a 2 year grace period before repayment begins except you have 10 years to repay the amount you took out.

VERY IMPORTANT- You will not receive a further tax deduction on repayments since you already received the tax deduction the first time around.

RRSP to FHSA

The First Home Savings Account (FHSA) was introduced in 2023. The contribution limit is $8000/year up to a maximum of $40,000. If you’re short on funds to contribute to the FHSA – a tax-sheltered transfer can be done from your RRSP to your FHSA. Please note that there is no tax deduction on the FHSA if a RRSP transfer is done.

Please do not hesitate to contact us if you have any questions about RRSPs or whether it makes more sense to consider TFSAs or FHSAs for your situation. If you know you will be topping up your RRSPs for the 2025 tax year, please get in touch with us BEFORE March 02, 2026.

E&OE

5 Questions into 2026 from Fidelity Investments

Is AI a bubble?

- The impact of AI will likely shape market direction in 2026, but it’s too early to say if it’s a true transformation or a temporary mania.

- Fidelity’s approach is to remain moderately overweight equities, favoring growth managers who can capitalize on AI trends, while controlling risk through selective short positions.

- Diversification is maintained, with investments in regions and sectors less dependent on AI, plus fixed income and alternatives for stability.

- Ongoing close collaboration with equity analysts ensures readiness to adjust positions if the earnings outlook changes.

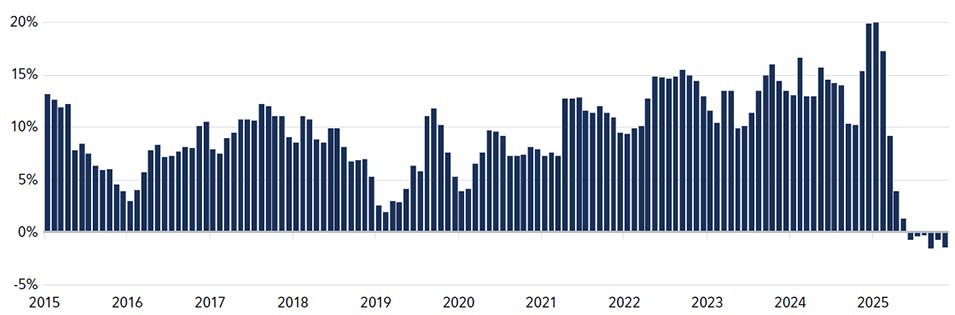

Exhibit #1 – Will AI indeed usher in a new era for earnings?

U.S. corporate profits as a % of GDP, including projection to 2030*

*2025-2030 projected using discounted cash flow model based on current market valuations.

Source: Bureau of Economic Analysis, Haver Analytics, FMR Co calculations. As of Jun. 30, 2025, Jul. 1, 2025 to Dec. 31, 2030 based on FMR Co calculations

What are your concerns around the U.S?

- Political risks—especially threats to Federal Reserve independence—could undermine the dollar’s global status.

- Fidelity has eliminated its long-standing overweight to the U.S. dollar, diversified into other currencies (euro, yen), and increased gold holdings as a hedge.

- Direct holdings of U.S. Treasuries have been reduced, with a shift toward more attractive opportunities globally, including renewed focus on Canada.

Exhibit #2 – Goodbye Greenback

Fidelity Global Balanced Portfolio vs. benchmark relative USD$ exposure, positive values reflect an overweight allocation

Source: Fidelity Investments, Bloomberg. As of Nov. 28, 2025

Things don’t feel great in Canada. Why do you sound optimistic?

- Canada’s fundamentals are improving: GDP growth rebounded, unemployment fell, and business optimism is rising.

- The Federal Budget’s focus on investment and productivity is a positive step, though execution risks remain.

- Fidelity has closed its underweight position in Canadian assets, capturing recent outperformance, and will consider further allocation based on ongoing economic trends.

Exhibit #3 – This needs to go up if Canada is to thrive

Cumulative % increase in total real gross fixed capital formation

Source: OECD, Haver Analytics. As of Dec. 31, 2024

How are you thinking about alternative asset classes and evolving the 60E/40F portfolio?

- Traditional stock/bond portfolios have become less efficient due to increased correlation, especially with inflation uncertainty.

- Fidelity has added both liquid and illiquid alternatives to client portfolios, including specialized long/short stock selection strategies and Canadian commercial real estate.

- The team’s research agenda for 2026 continues constantly evaluating new alternative strategies to enhance diversification and long-term returns.

Exhibit #4 – Stocks and bonds now moving together

Correlation between S&P 500 and U.S. Treasury Bond Index

Source: Bloomberg, rolling 40-month correlation of S&P 500 and Bloomberg U.S. Treasury Index. As of Nov. 2025

How are you approaching the recent rise in geopolitical risk?

- Geopolitical risks are unpredictable, but Fidelity’s disciplined asset allocation process focuses on policy impacts, not politics.

- Risk management remains a priority, with gold held as a hedge against geopolitical uncertainty.

- Team is prepared to adjust portfolio positioning quickly and decisively if conditions warrant.

Key Takeaways

- AI’s market impact is uncertain, but Fidelity remains cautiously optimistic. The team is moderately overweight equities, focusing on growth managers who can benefit from AI trends, while maintaining diversification and readiness to adjust if the earnings outlook changes–stock prices follow earnings.

- Political and currency risks in the U.S. have prompted a shift in strategy. Fidelity has reduced exposure to USD$ and Treasuries, diversified into other currencies and gold, and is seeking more attractive opportunities globally, including Canada.

- Canada’s improving fundamentals and policy focus support a constructive outlook. Recent economic data and the Federal Budget aimed at investment and productivity have led Fidelity to close its underweight in Canadian assets, with further allocation dependent on ongoing trends.

Source: Fidelity Investments

Value of an Advisor – More than a Guide

A trusted advisor helps navigate the complexities of wealth, paving the way for generations to come. This simple and handy formula helps you understand the value of working with an advisor.

Source: Russell Investments

YouTube Video Feature: Most Canadians miss this costly tax drag on investments

Most Canadians believe market volatility is the biggest risk to their non-registered investments. In reality, the real threat is much quieter – annual tax drag that steadily erodes after-tax returns, even when markets perform well. Once RRSPs and TFSAs are maximized, every additional dollar invested becomes exposed to ongoing taxation. Over time, the tax drag can quietly reduce long-term wealth by six figures without any obvious mistake being made.

Corporate class investing is one of the few strategies designed to address this problem, but the advanced benefits are rarely explained clearly. When structured properly, corporate class funds can help defer tax, improve compounding efficiency, manage retirement income and reduce exposure to OAS clawbacks. This is especially true for high-income investors and business owners with retained earnings.

This discussion walks through how tax deferral impacts compounding, how corporate class functions inside a corporation, common misconceptions and how this structure can help control taxable income throughout retirement. If you care about after-tax results and not just headline returns, understanding how your non-registered investments are structured is critical.

E&OE

DLD in the Media

- Money-Savvy Pig: How a simple system is teaching my kids financial wisdom – Financial Advice for All – Advocis

- True or False: You’ll save more when you earn more – Neo Financial

- Small monthly changes can add up over the year to help boost savings – The Canadian Press

Please do not hesitate to contact us if you have any questions or if there’s anything we can do to help. Thank you for your time and from all of us at DLD.

Warmest regards,

Dave, Kelly, Ryan, Aaron and Ian

E&OE